SIMBA Telecom just announced it’s latest Financial report and indicated a few keypoints.

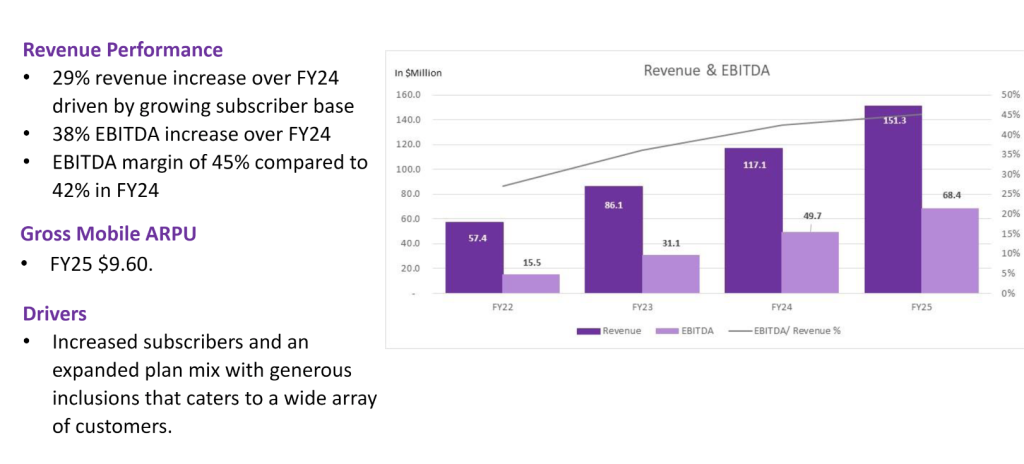

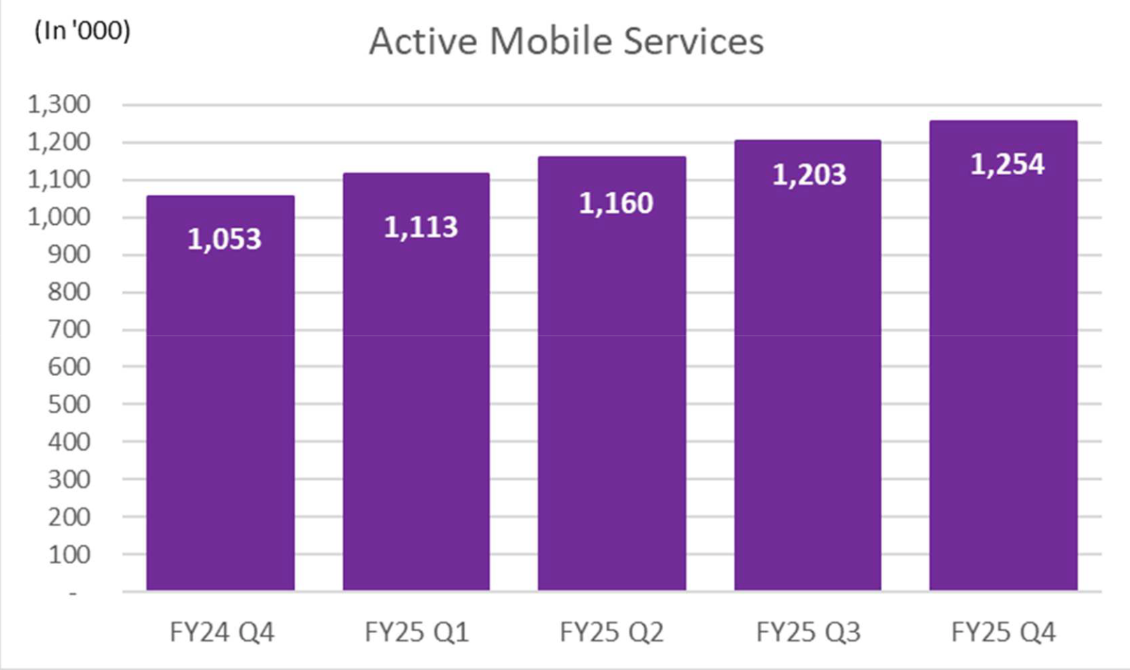

Subscriber base has increase again to 1.254 million. Simba achieved a gross mobile ARPU of S$9.60. This does not include interconnect revenues which have been growing with Simba’s larger subscriber base.

Simba continued to grow its mobile network in Singapore, upgrading 474 sites to deliver more

capacity and 5G services in key areas to customers. In addition, Simba has been leveraging the

latest network technology to improve network performance and use real-time analytics for more

eGicient planning and execution.

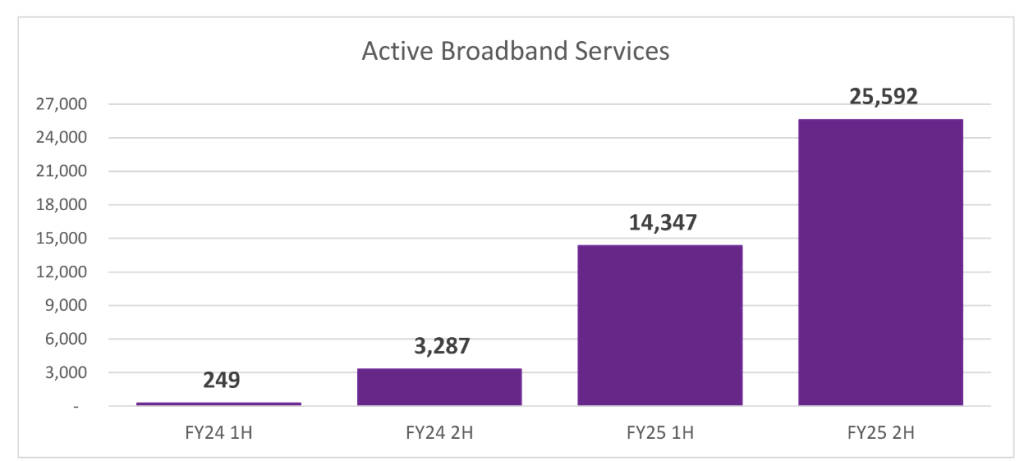

As for fibre broadband, it increased it’s subscriber base to 25,600 customers.

As for M1 acquisition, TUAS will employ a two-brand strategy, with Simba continuing to work

hard providing the best value plans in the Singapore market, while M1 continues to focus on

more premium style customer service.

The necessary Long Form Consolidation Joint Application has been submitted to IMDA and

Tuas hopes to receive regulatory approval for the acquisition over the next few months

Simba will continue to be focused on growing its share of the home broadband market and this

should yield additional revenues for the business.

The acquisition of M1 is subject to a number of conditions including regulatory approvals by the Singapore Infocomm Media Development Authority.

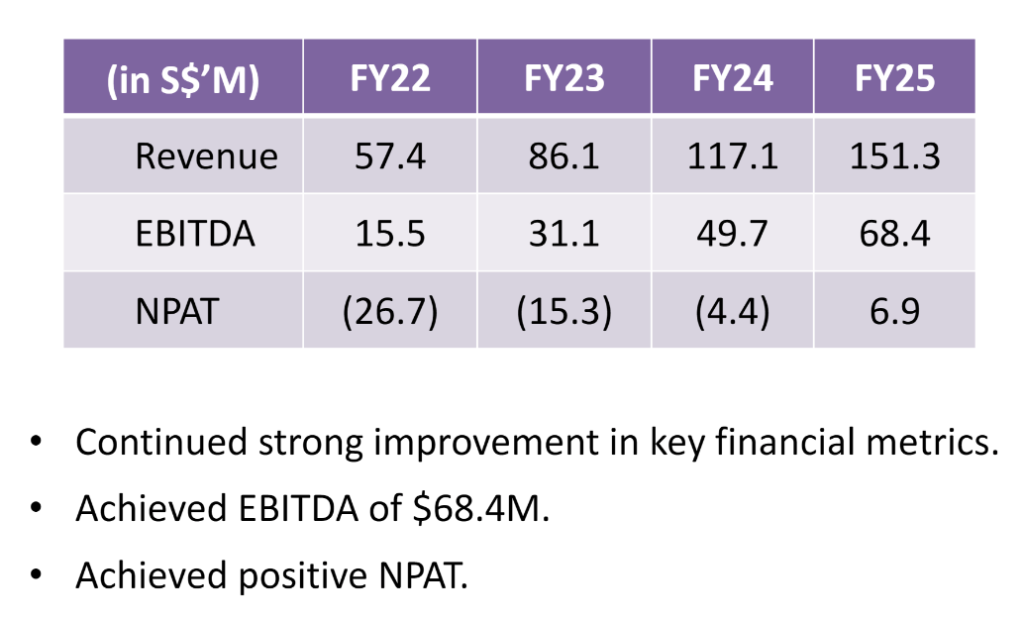

As for financial results, it has acchieved net profit after tax of 6.9 million.